The Asian Development Bank’s March 2013 edition of the Pacific Economic Monitor covers the growth outlook for Pacific island economies as well as topical policy issues. Here are the agricultural parts and other interesting information presented for context.

Overview

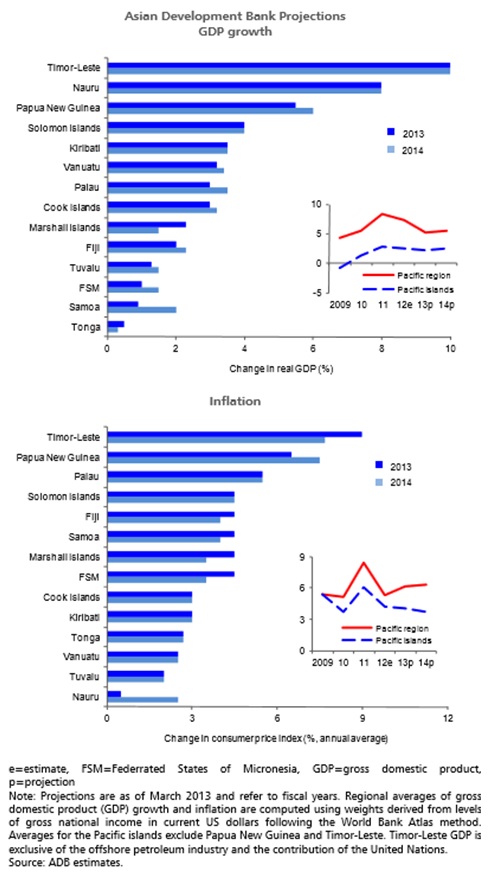

“Economic growth in the Pacific moderated to 7.3% in 2012, from a post-crisis high of 8.3% recorded in the previous year. This regional trend was driven primarily by the performance of the region’s larger, natural resource–extracting, economies. Growth slowed slightly, but remained high in Papua New Guinea (PNG) and Timor-Leste. Economic growth in the Pacific islands also moderated to 2.5% in 2012, from 2.8% a year ago. Growth in Solomon Islands moderated from double-digit rates as log revenues leveled off. Economic stimulus from infrastructure projects was lower in Kiribati, the Federated States of Micronesia, Samoa, and Tonga.”

“Inflation moderated to 5.3% in 2012 from 8.5% in 2011 as international food and fuel prices stabilized, albeit at high levels.”

“The value of Pacific exports to New Zealand increased by 2.5% in 2012 compared with 2011, supported by greater exports from Nauru (phosphate) and PNG (coffee and food products). Fiji’s exports of agricultural products to New Zealand fell by 11% during the same period, partly reflecting lower sugar production”.

Fiji

“Latest official estimates, as contained in the 2013 Budget, are that GDP growth picked up to 2.5% in 2012. The Reserve Bank of Fiji reports that new lending for consumption and investment increased by 25.4% and 28.1%, respectively, last year. There has been a steady buildup in private sector credit, with lending up by 4.7% through December 2012.”

“Performance of some sectors of the economy worsened relative to 2011. Sugar production fell 7.1%, reflecting weak global demand and the impact of floods early in the year. Gold production also fell by 8%, but bauxite production remained buoyant. Tourist arrivals declined by 2.1% in 2012. December arrivals were driven down due to flight cancellations caused by Cyclone Evan. The cyclone caused an estimated $42 million (about 1% of GDP) in damage, just under half of which was to the non-sugar agriculture sector. Given these developments in key sectors, 2012 growth estimates are likely to be adjusted downward.

“Floods in early 2012 contributed to higher inflation in the first few months of the year. For the year as a whole, inflation was 4.3%— less than half of the rate in 2011.”

“Despite significant investments in recent years, the outlook for Fiji’s sugar industry remains uncertain. In 2012, 20% of mature sugarcane sustained damage due to natural disasters, which will impact on sugar output this year. The recent government announcement that it will purchase mechanized equipment to raise production efficiency may not be sufficient to overcome the industry’s challenges in its efforts to competing internationally. There is a need to embark on deeper structural adjustment. Ongoing negotiations around the contract price of sugar are likely to result in a lower price owing to the global supply glut.”

“Fiji’s growth performance over the medium term faces a number of challenges. While new investments and signs of greater interest from investors are encouraging, actual realization of foreign investment will be impacted by the country’s political situation. The country’s vulnerability to natural disasters and limited fiscal space (due to current debt level) are factors also constraining growth prospects.”

“Recent enhancements in Fiji’s social welfare system will improve targeting and coverage of the vulnerable, enabling it to benefit nearly 13,000 poor households. This will expand coverage from the current 3% to 10% of the population. This level of commitment to protecting the vulnerable puts Fiji at the forefront of development of social safety nets in the Pacific.”

Federated States of Micronesia

“Inflation rose in FY2012 on the back of higher global prices for food and fuel, and credit expansion. Costs of food and fuel, which together make up about half of the average consumption basket in the Federated States of Micronesia (FSM), were elevated during the early part of the fiscal year.”

Palau

“Growth remained relatively robust, albeit with some moderation, in FY2012 (ended 30 September) due to the continued strong performance of the tourism sector. Visitor arrivals again grew at a double digit rate, the third consecutive year of high growth, on the back of increasing number of tourists from Japan, Taipei,China, and Republic of Korea.”

“The moderation in arrivals and GDP growth is expected to continue through FY2013. Growth in FY2014 is dependent on the government’s forward investment plans. Easing global supply conditions for food and fuel are projected to result in declining inflation over the next two years.”

Papua New Guinea

“In 2012 PNG was one of the fastest growing economies in Asia and the Pacific with near double-digit growth. The non-mineral sector performed most strongly, led by construction, transport, finance, and retail trade, as domestic demand created by the building of a liquefied natural gas (LNG) project reached its peak. Mining output recovered from technical disruptions and unfavorable weather experienced in 2011. Government expenditure was higher than expected. Falling oil output due to declining reserves dragged down overall growth. Growth in agriculture, forestry, and fisheries output slowed as a result of poorer growing conditions and moderating export prices, which led to lower coffee, copra, and cocoa output.”

“Economic growth is projected to ease to 5.5% in 2013, as the scaling down of LNG project construction reduces construction and transport activity, with spillovers to other sectors such as retail and wholesale trade. Moderating prices of key agricultural exports and a strong kina are expected to depress rural incomes and consumption.”

Samoa:

“Economic growth moderated to 1.2% in FY2012 (ended 30 June) from 2.0% in the previous year. Samoa experienced lower growth over the past year as reconstruction and rehabilitation following the 2009 tsunami wound down.”

“In the first quarter of FY2013, GDP growth picked up, reaching 2.1% (y-o-y) supported by the manufacturing sector. However, at the end of the second quarter, Cyclone Evan hit, causing damage estimated at more than $210 million (equivalent to around 30% of GDP). Agriculture and tourism were the hardest hit, incurring losses estimated at $28 million each. Transport, power, and water and sanitation infrastructure also suffered significant damage, as did school buildings and housing. Restoration of production capacity and reconstruction of essential infrastructure are expected to take about 2–3 years”

“Inflation rose to 6.2% in FY2012, largely driven by higher food prices. Over the first half of FY2013, inflation has been on a declining trend, with deflation recorded in every month from September to December 2012”

“Growth is now projected at 0.9% for FY2013. This reflects declining output from agriculture, tourism, and other productive sectors due to infrastructure damage caused by Cyclone Evan. Economic recovery efforts, once fully in place, are expected to have a positive impact on GDP in FY2014, with projected growth of 2%.”

“Inflation can be expected to rise over the second half of FY2013 with higher domestic food prices arising from supply disruptions. Full year inflation is now projected at 4.5%, and is seen to slow to 4.0% in FY2014 in line with declining international food and fuel prices, and restoration of the distribution network.”

Solomon Islands:

“Growth slowed to 5.5% in 2012, from 10.6% in the previous year, due to declines in agriculture and steady forestry output. Log production remained at 2011’s record levels due to strong external demand and higher investment in the sector. Production of cocoa and copra slumped due to sluggish demand overseas.”

“Falling international prices of logs (by 7.7% in 2012) and agricultural commodities reduced export revenues and generated a trade deficit in the second quarter of 2012—the first after 4 consecutive quarters of trade surpluses.”

“Growth is expected to slow further, to 4%, in 2013. Although agricultural production and gold output are projected to increase, log production is seen to decline.”

“Due to a lag observed in the effect of changes in international prices on the Solomon Islands economy, international food price rises from mid-2012 are expected to impact inflation in early 2013, but to dissipate by midyear. Over full-year 2013, average inflation is expected to ease to 4.5% as economic growth slows.”

“Logging accounts for 15% of government revenue, 60% of exports, and 32% of foreign exchange earnings. It is the largest source of formal sector employment (second only to the government), accounting for about 5,000 jobs. Forests have been extensively exploited—logging rates have been estimated to have reached several times the sustainable rate in recent years. One study warns that natural forest resources may be exhausted before 2020. A decline in logging would adversely impact government finances and necessitate new sources of government revenues (e.g., a new taxation regime for the mining sector) to maintain government expenditures.”

Tonga

“Growth slowed considerably in FY2012 (ended 30 June), falling to 0.8% from 2.9% in the previous year. Weak remittances and declining private sector borrowing, along with the completion of large development partner-financed public investment projects, weighed down growth.”

“Inflation fell to 4.6% in FY2012, down from 6.1% in FY2011. Winding down of infrastructure projects and weak domestic activity relieved pressures on domestic prices, despite slight rises in international food and fuel prices during the fiscal year.”

Tuvalu

“After contracting in 2009–2011, the economy expanded by 1.2% in 2012 due to continued growth in development spending and retail trade. Inflation also accelerated in 2012, driven by higher transport prices as well as higher food prices early in the year.”

Vanuatu

“The economy is estimated to have grown by 2.0% in 2012 on the back of recovery in the tourism sector. Following 2 years of decline, tourist arrivals increased by about 15% in 2012, largely due to higher arrivals from major markets (Australia and New Zealand). The hosting of the African Caribbean Pacific/European Union Conference also increased visitor arrivals and provided a small boost to construction activity.”

“The agriculture sector, which accounts for 23% of the economy, contracted (through the first 3 quarters of 2012) due to declines in the production of kava, beef, and coconut oil. Although copra production increased by a third in 2012, it only accounts for about 5% of the agriculture sector.”

“Coming from a 0.9% increase in the consumer prices in 2011, inflation is estimated to have increased to 1.4% in 2012— driven by higher food prices early in the year. Consumer prices trended lower during the second and third quarters of the year driven by food and utility price falls.”

“Growth is expected to pick up to 3.2% in 2013 and 3.4% in 2014, as delayed construction projects begin to be implemented and agricultural production recovers. Tourist arrivals are also expected to grow in 2013, partly due to diversion of visitors from Fiji due to Cyclone Evan.

“Economic growth has slowed significantly in recent years. The economy grew by 6.5% in 2008 compared with an average of 2.1% in 2009–2011. The completion of large development partner-funded projects and declining property investment fueled this decline. Expanding the economic and export bases, and development of better infrastructure to facilitate easier movement of goods and persons, should help support economic growth and job generation moving forward.”